EU-MERCOSUR: a strategic agreement in a more volatile trade environment

After more than two decades of negotiations, on 6 December 2024, the EU and the MERCOSUR countries concluded the negotiation process for the agreement that lays the foundations for a strategic partnership (Council of the European Union 2026a). The next step came in January 2026, when the Council authorised the signing on 9 January, and the agreement was officially signed on 17 January 2026 in Asunción, Paraguay (Council of the European Union 2026b).

In a context of increased geopolitical rivalry and trade uncertainty, the European Union (EU) is seeking to strengthen alliances that provide scale, stability and access to resources and markets. This is the context in which the political momentum behind the EU-MERCOSUR trade agreement can be understood, combining trade objectives with a clearly strategic approach.

Even so, the signing does not mean that the agreement will enter into force. The agreement now enters its most sensitive phase, that of ratification, where much of the political debate will be concentrated. In the European Union, the next milestone is the consent of the European Parliament and then formal adoption by the Council. From there, and depending on how it is legally articulated, the strictly commercial part could be applied more immediately through an interim instrument, while the broader partnership framework, which also incorporates political and cooperation components, would require additional ratifications at the Member State level (Council of the European Union 2026a).

At the same time, in the MERCOSUR countries, the agreement must be submitted for parliamentary approval in each State party, so that the final timetable will depend on institutional developments in both blocs (Council of the European Union 2026a).

At this point, the agri-food component has become the main focus of controversy and political pressure within the EU. Agricultural organisations and some governments have expressed concern about the possible increase in imports of sensitive products and the risk of competitive asymmetries if effective reciprocity in standards and controls is not guaranteed, particularly in the use of certain plant protection products, environmental requirements and working conditions.

This response is having a practical impact on the ratification debate, raising the political cost of moving forward with the timetable and reinforcing the demand for protective instruments, such as tariff quotas on sensitive products, enhanced monitoring and safeguards that can be activated in the event of market disturbances.

In recent days, the timeline has become more uncertain. On 21 January 2026, the European Parliament decided to refer the EU-MERCOSUR agreements to the Court of Justice of the EU for a ruling on their compatibility with the Treaties, in particular due to doubts linked to the rebalancing mechanism and its possible impact on European regulatory autonomy (European Parliament 2026). This decision paralyses the progress of parliamentary consent until a judicial ruling is issued and could significantly lengthen the process , with estimates pointing to a potential delay of close to two years (Reuters 2026).

Despite this scenario, the agreement maintains a broad economic scope and reinforces the message of commitment to rules-based trade (Grieger 2025). Its main measures include:

- The phasing out of tariffs on more than 90% of traded products.

- Improved market access for European companies and investments.

- Promotion of sustainable access to raw materials.

- Integration of value chains between both regions.

- Inclusion of commitments on sustainable development, climate change and labour rights.

In practical terms, the agreement provides for the gradual elimination of tariffs on more than 90% of traded goods, which will particularly benefit Spanish sectors such as industry and agri-food. MERCOSUR currently applies high tariffs on European products—up to 35% on cars and 50% on fruit—the removal of which would facilitate the entry of Spanish companies into a strategic market with high potential (European Commission n.d.a; Grieger 2025). In the case of agri-food, the opening up of the market is more selective for sensitive products through quotas and safeguard mechanisms, a key aspect for understanding the current sectoral debate in the EU (European Parliament 2025).

Although the agreement has not yet entered into force, trade relations between the EU and MERCOSUR are based on a solid and sustained foundation (Illustration 1). MERCOSUR is, in fact, the EU’s tenth largest partner in trade in goods, and the EU remains the Latin American bloc’s second largest partner, behind only China. In 2024, the EU accounted for around 17% of MERCOSUR’s total trade, a share that has been recovering since the post-pandemic reopening (European Commission n.d.b).

Illustration 1. EU-MERCOSUR exports and imports

(*) Cumulative data from January to November

Source: own elaboration based on Eurostat data

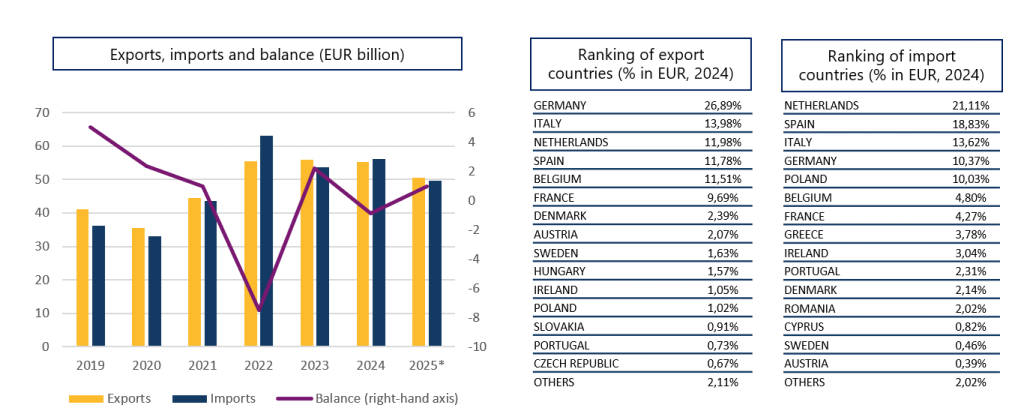

With final data for 2024, European exports to MERCOSUR stood at around €55 billion, while imports reached approximately €56 billion. The most recent reading, with cumulative data from January to November 2025, points to a similar dynamic, with EU exports to the bloc at €51 billion and imports at €50 billion.

By country, Brazil remains the leading partner, accounting for more than 80% of trade flows between the two blocs and well ahead of Argentina, Uruguay and Paraguay, a position consistent with its economic weight and natural resource endowment.

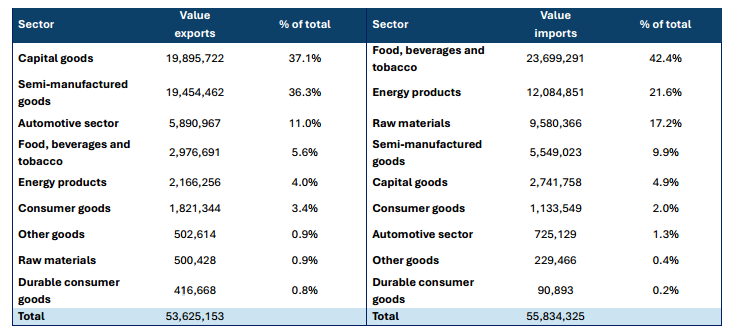

In terms of sectoral composition, in 2024 the EU mainly exported capital goods (37%), semi-manufactured goods (36%), and automotive products (11%) to MERCOSUR, as shown in Table 1. Conversely, imports from MERCOSUR were mainly concentrated in food, beverages, tobacco, energy products and raw materials, with Brazil and Uruguay as the main suppliers in these segments.

Table 1. Main EU-MERCOSUR export and import sectors in 2024 (in thousands of euros)

Source: own elaboration based on data from the Ministry of Economy, Trade and Business

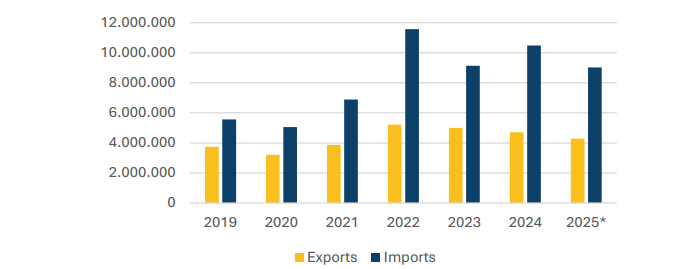

The formalisation of the agreement between the EU and MERCOSUR would benefit the entire Union, but its strategic impact would be particularly significant for Spain, which ranks sixth among European exporters and second among importers in its relations with MERCOSUR (Statistics Netherlands 2025). As the EU’s leading agricultural exporter, Spain could consolidate its position as a key bridge in trade between Latin America and Europe, aided by the reduction of trade barriers. This would strengthen already significant trade relations, which have shown positive growth in both exports and imports in recent years (Graph 1).

Graph 1. Evolution of the value of exports and imports between Spain and MERCOSUR (in thousands of euros)

(*) Cumulative data from January to November

Source: own elaboration based on data from the Ministry of Economy, Trade and Business

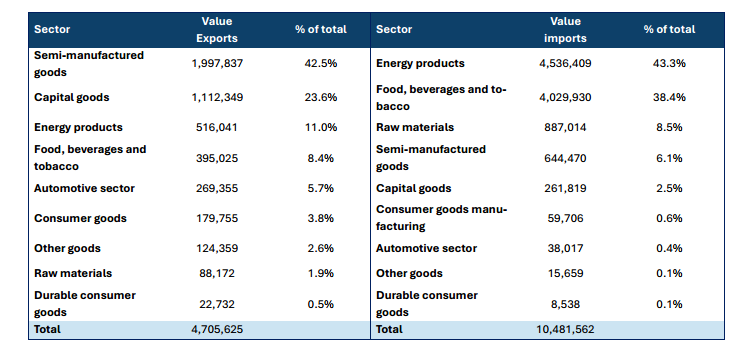

By sector, and as shown in Table 2, Spanish exports are led by semi-manufactured goods, capital goods and energy products. In terms of imports, energy products, food and raw materials stand out, with Brazil as the main trading partner.

Table 2. Main export and import sectors between Spain and MERCOSUR in 2024 (in thousands of euros)

Source: own elaboration based on data from the Ministry of Economy, Trade and Business

At the same time, the agri-food sector accounts for much of the reluctance and complaints from the sector in the EU and Spain. Agricultural organisations warn of possible competitive imbalances if trade liberalisation is not accompanied by effective reciprocity in standards and controls, especially in areas such as the use of plant protection products, environmental requirements and working conditions. This pressure is already influencing the political debate on the agreement, reinforcing the demand for mitigation mechanisms for sensitive products, with quotas, enhanced monitoring and the activation of safeguards when market disturbances are detected.

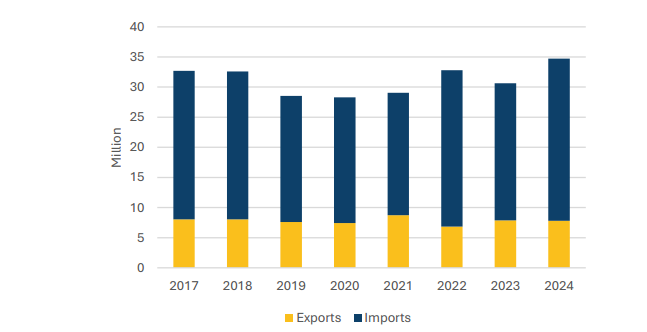

One of the areas where the agreement between the European Union and MERCOSUR could have the greatest impact is in port traffic and maritime services. The intensification of trade flows between the two blocs could consolidate Spanish ports as key logistics hubs on the South Atlantic axis, generating new opportunities for economic development and maritime connectivity.

According to data from Puertos del Estado, between 2017 and 2024, the volume of goods handled by Spanish ports in their trade with MERCOSUR countries has shown remarkable stability (Graph 2). Imports have remained at around 23 million tonnes per year, peaking at over 26 million in 2024. Exports, meanwhile, have fluctuated between 6.8 and 8.7 million tonnes. These figures reflect the structural importance of trade with this region, as well as its growth potential if barriers are reduced and logistics exchanges are streamlined.

Graph 2. Trend in Spain–MERCOSUR port traffic in million tonnes (including transshipment) (2017–2024)

Source: own elaboration based on data from Puertos del Estado

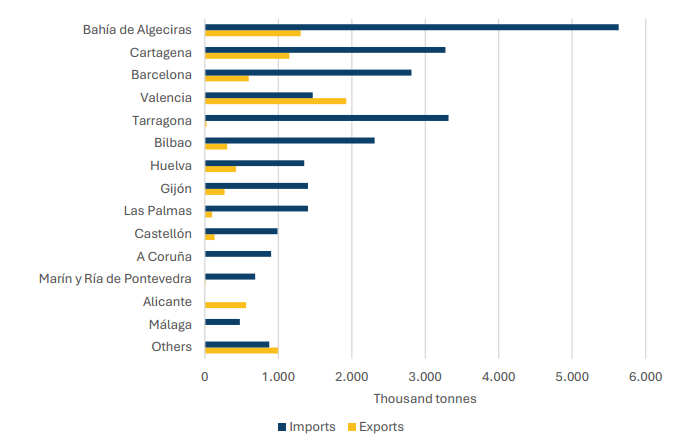

Furthermore, according to the latest data available for 2024, trade with MERCOSUR is not concentrated in a single enclave, but is distributed among various ports of general interest, demonstrating the capillarity and resilience of the Spanish port system. As shown in Graph 3, the Port of Valencia led exports to MERCOSUR with more than 1.9 million tons, while Bahía de Algeciras and Tarragona were the main points of entry for goods from this region, with 5.6 million and 3.3 million tons, respectively.

Graph 3. Main Spanish ports in trade with MERCOSUR in thousands tonnes (including transhipment) (2024)

Source: own elaboration based on data from Puertos del Estado

This territorial distribution represents a competitive advantage over other European countries, as it allows for route diversification, reduces bottlenecks and takes advantage of synergies between different logistics corridors. If the agreement is successfully implemented in operational terms, it could result in a strengthening of regular maritime services, more frequent port calls and increased intermodal connectivity, thus consolidating the role of Spanish ports as logistics platforms between Europe and South America.

At the same time, it should be borne in mind that part of the potential increase in trade would be concentrated in agri-food products, precisely the area with the greatest social and regulatory sensitivity. In this case, port operations could be affected by increased sanitary and phytosanitary controls, cold chain management and traceability requirements, factors that influence times, costs and logistics planning.

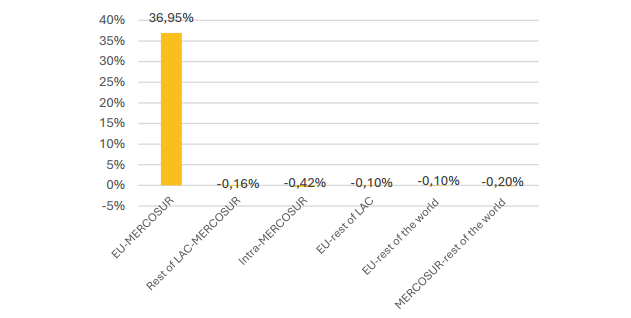

Beyond these tangible effects on logistics chains and maritime services, the EU-MERCOSUR agreement has a marked strategic component in both economic and geopolitical terms. According to an analysis by the Elcano Royal Institute, its implementation could result in an increase in bilateral trade of up to 37% (Graph 4). This figure could rise to 70% if technical instruments such as cross-accumulation of rules of origin or Mutual Recognition Agreements (MRAs) are applied, which consists on mechanisms that relax technical requirements in key sectors such as pharmaceuticals, agri-food and industry.

Graph 4. Change in trade flows between geographical regions following the ratification and entry into force of the EU-MERCOSUR agreement (% variation, average exports and imports)

Source: Elcano Royal Institute, 2025

In addition to strengthening transatlantic trade, the agreement could also act as a catalyst for intraregional trade in Latin America. Current estimates suggest that, if the EU-MERCOSUR agreement is used as a platform to interconnect rules of origin and facilitate regional value chains, intraregional trade in Latin America could increase by up to 38% (Berganza et al. 2025). In this scenario, the EU would consolidate a network of trade agreements in the region covering around 95–97% of Latin American GDP (Cornejo et al. 2025). The result would be a bi-regional economic area of around 1.1 billion people, with an aggregate GDP comparable to that of the United States.

In this context, the trade agreement between the European Union and Canada (CETA) serves as a useful reference for anticipating possible effects. Since its provisional application in September 2017, CETA has eliminated 98% of tariff lines and will complete the reduction to cover 99% by 2024. At the same time, EU-Canada trade has shown significant progress, with growth of around 65% in goods between 2016 and 2024 and close to 90% in services. In terms of positioning, the EU remains Canada’s second largest trading partner in goods, behind only the United States and ahead of China (Council of the European Union 2025).

However, the experience of CETA also shows that the leap from provisional application to full ratification can be lengthy. To date, the national ratification process remains incomplete in several Member States and continues to be a politically sensitive issue (European Commission n.d.c). The case of France is illustrative, with the Senate rejecting ratification in March 2024 amid social pressure from the agricultural sector and debate over competition and standards (Reuters 2024). This precedent suggests that, even with demonstrable trade benefits, the domestic political process can influence the timing and stability of the agreement.

In terms of lessons learned, the comparison reinforces the importance of accompanying these agreements with clear regulatory frameworks, monitoring mechanisms and operational safeguards, as well as sustained dialogue with the most exposed productive sectors. This fine-tuning is often crucial to maintaining internal consensus and reducing uncertainty during the transition.

In the case of the EU-MERCOSUR association agreement, Spain is in a particularly favourable position due to its export network, logistics infrastructure and maritime connectivity. With gradual and predictable trade liberalisation, the combination of these factors could translate into sustained growth in trade and greater investment associated with transatlantic supply chains.

In addition to this context, there is an external factor that has regained importance in recent months. The United States’ tariff shift, with announcements of widespread tariffs from 2025 onwards, has increased uncertainty and reactivated market diversification strategies (Rubin 2025). At the same time, various institutions have adjusted their forecasts for Latin America and the Caribbean in an environment of increased trade friction, with downward revisions in highly exposed economies such as Mexico and, to a lesser extent, Brazil (Campos 2025).

In the case of Mexico, some estimates have placed 2025 growth at around 0.6% in scenarios of tariff tension (Forbes Staff 2024). For Brazil, the debate has focused on the impact of new trade measures and their effect on specific sectors, with references to tariffs applied by the US on Brazilian imports and products such as steel (Sá Pessoa 2025).

Given this scenario, the ratification of the EU-MERCOSUR agreement gains strategic relevance for a very practical reason: to expand commercial manoeuvring room and reduce dependencies at a time of regulatory volatility. Beyond the direct boost to bilateral trade, the agreement would also provide a more stable framework for guiding investment, value chains and logistical decisions in the Europe-Latin America axis.

References

- BERGANZA, J.C. [et al.]. 2025. EU-MERCOSUR: a platform for a new era of transatlantic and intra-regional Latin American integration? Elcano Royal Institute, Analysis. 14 January 2025 [online]. Available at: https://www.realinstitutoelcano.org/analisis/ue-mercosur-plataforma-hacia-una-nueva-era-de-integracion-transatlantica-e-intrarregional-latinoamericana/ [Accessed: 22/01/2026].

- CAMPOS, R. 2025. IMF cuts Latam, Caribbean 2025 GDP growth estimate. Reuters, 22 April 2025 [online]. Available at: https://www.reuters.com/world/americas/imf-cuts-latam-caribbean-2025-gdp-growth-estimate-2025-04-22/ [Accessed: 22/01/2026].

- EUROPEAN COMMISSION. n.d.a. Factsheet: EU-Mercosur Partnership Agreement – Opening a wealth of opportunities for people in Spain [online]. Available at: https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/mercosur/eu-mercosur-agreement/factsheet-eu-mercosur-partnership-agreement-spain_en [Accessed: 22/01/2026].

- EUROPEAN COMMISSION. n.d.b. Mercosur. EU trade relations with Mercosur [online]. Available at: https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/mercosur_en [Accessed: 22/01/2026].

- EUROPEAN COMMISSION. n.d.c. Canada. EU trade relations with Canada. Facts, figures and latest developments [online]. Directorate-General for Trade and Economic Security. Available at: https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/canada_en [Accessed: 22/01/2026].

- *Consult the downloadable document for the complete list of bibliographic references.

*Disclaimer: This English version has been generated with the support of AI-based translation tools. In case of discrepancies, the Spanish original prevails.