R&D&I as a financial leverage for the port sector

1. Investment in R&D&I as a Driver of Resilience

In the contemporary global economy, investment in R&D&I has established itself as the definitive metric of resilience and sustainable growth. However, an analysis of the data from the 2025 EU Industrial R&D Investment Scoreboard (European Commission 2025) reveals a critical disparity in the innovative efforts undertaken by different European industrial sectors.

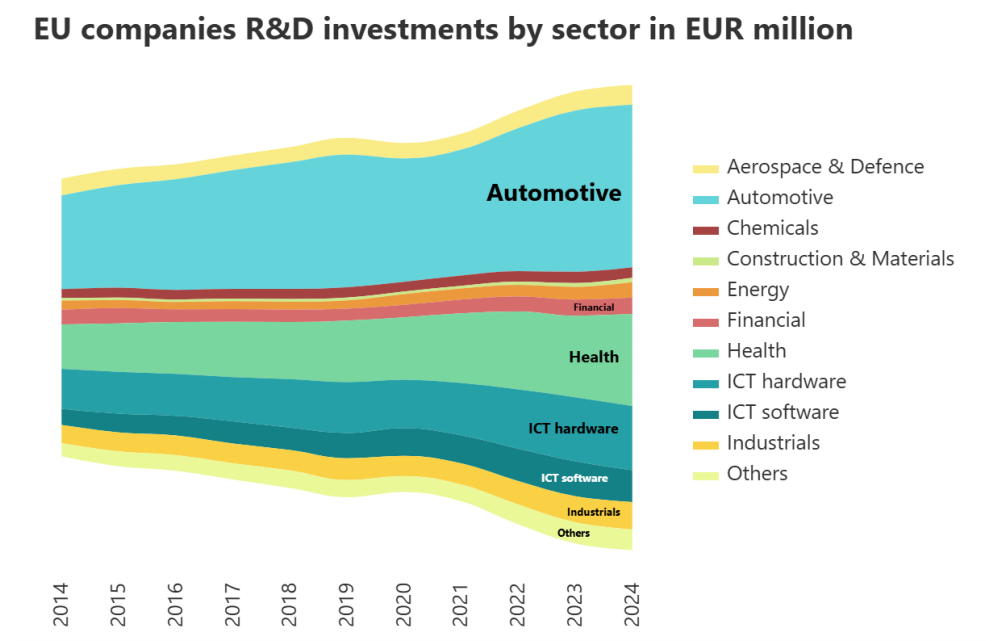

Whilst sectors such as the automotive industry, healthcare (pharmaceuticals and biotechnology) and ICT services lead the European rankings in terms of R&D intensity (investing between 12% and 15% of their revenue respectively), the transport and logistics sector exhibits a significantly lower intensity. Specifically, the maritime and port transport sector has historically maintained investment levels below 1%, placing this sector in the position of a ‘technological follower’ compared to other high-intensity industries.

Illustration 1. EU industrial R&D investment by sector in millions of euros (top 800 EU) (Transport and logistics are included within the ‘Industrials’ category)

Source: 2025 EU Industrial R&D Investment Scoreboard

This investment gap in Europe, and particularly in Spain, reveals untapped growth potential. The Spanish port system, which handles 80% of the country’s foreign trade, faces decarbonisation and digitalization challenges that demand a profound transformation. The opportunity for companies in the sector lies in breaking this trend of low investment by adopting a proactive strategy that leverages public funding frameworks and tax incentives to turn technological expenditure into a high-return financial asset.

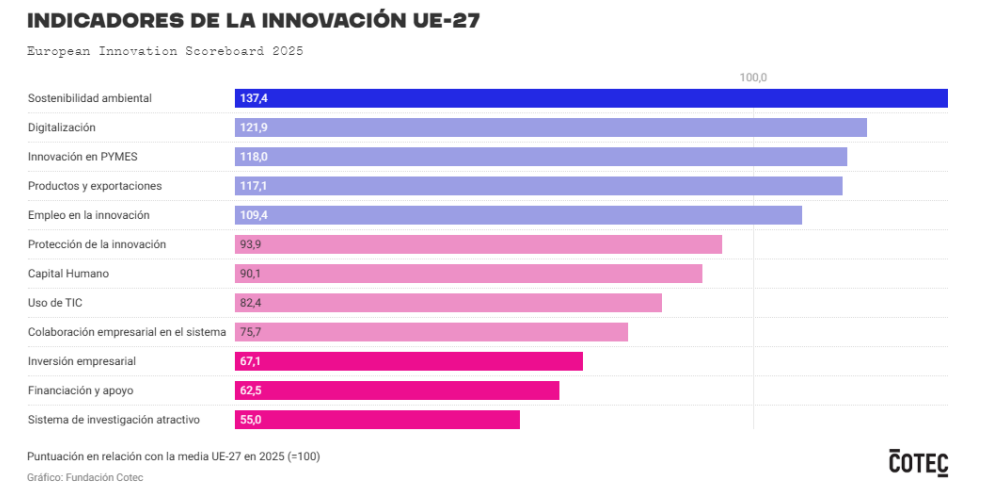

Illustration 2. Spain’s position relative to the EU average in innovation indicators

Source: COTEC Foundation

2. Drivers of Disruption: AI, Decarbonisation and Digitalization

The transformation of the maritime and port sector is currently centred on three key areas that have evolved from mere trends into the main drivers of R&D&I projects. With estimated investment in disruptive technologies for the logistics sector set to exceed €15 billion annually worldwide by 2027 (according to MARKETSANDMARKETS), the implementation of these drivers enables traditionally operational processes to be classified, both technically and for tax purposes, as high value-added projects. These investments, when properly structured, can yield tax returns of between 12% and 42%, transforming technological expenditure into direct financial savings.

Artificial Intelligence (AI) as a transformative factor

AI has established itself as the brain of modern logistics. Investment in port AI solutions is estimated to grow at a compound annual growth rate (CAGR) of 23% until 2030. As these projects involve the creation of proprietary algorithms or significant adaptations to specific environments, they qualify for the highest tiers of tax incentives.

Examples of applications in the port sector:

- Predictive maintenance

- Optimisation using digital twins

- Machine vision and security

Decarbonisation as an engineering and sustainability challenge

Regulatory pressure (Fit for 55) has turned the energy transition into a driver of R&D&I, with planned investments in green port infrastructure in Europe reaching €10 billion for this decade. These projects involve innovation typically classified as R&D or IT depending on their technological risk, allowing for maximum tax deductions.

Examples of applications in the port sector:

- Electrification and OPS (Onshore Power Supply)

- Alternative fuels and green hydrogen

- Energy efficiency in infrastructure

Comprehensive digitalization and the data economy

Digitalization goes beyond simply replacing paper; it involves creating an ecosystem that generates exploitable intangible assets. Investment in port digitalization and Smart Ports is forecast to reach €5.5 billion annually by 2028, representing a massive tax base for the application of IT tax deductions (12%).

Examples of applications in the port sector:

- Blockchain platforms and PCS (Port Community Systems)

- Process automation (RPA)

- Cybersecurity in operational environments (OT)

3. Return on investment: revenue and tax efficiency

Despite the investment indicators mentioned, the commitment to technology and sustainability should not be viewed solely as an operating expense (OPEX). On the contrary, it is established as a strategic asset whose direct financial return is achieved through two complementary channels: the attraction of public funds and the optimisation of the tax burden.

However, it is imperative to emphasise that these financial incentives are not an end in themselves, but rather add to the intrinsic added value of innovation. If successful, technological implementation generates a distinctive competitive advantage—through process efficiency, reduced energy costs and market positioning—transforming the project into a high-return investment where tax savings and grants act as multipliers of operational success. The following sections will detail these last two channels of return.

Revenue through grants and public aid programmes

The current funding ecosystem offers a favourable environment for the logistics-port cluster, with instruments designed to mitigate the risk inherent in innovation. Among the most relevant funding mechanisms, the following stand out:

- Ports 4.0 Fund (Puertos del Estado): established as the main instrument for open innovation in the Spanish port system, this fund subsidises up to 80% of the costs of pre-commercial projects, facilitating the scaling of disruptive solutions from concept to real-world implementation.

- CDTI (Centre for Technological Development and Innovation): provides grants and subsidised loans for R&D projects, including non-repayable components of up to 33%, representing a direct injection of non-repayable capital into the company.

- European programmes (Connecting Europe Facility – CEF and Horizon Europe): these strategic funding frameworks are essential for large-scale projects aimed at decarbonisation and the roll-out of smart, interoperable infrastructure. The CEF programme typically offers grant rates ranging from 30% to 50% of eligible costs for transport and energy infrastructure, rising to 85% in cohesion contexts or for projects of particular cross-border interest. Meanwhile, Horizon Europe, the EU’s main research and innovation programme, offers higher funding rates: up to100% of direct costs for Research and Innovation Actions (RIA) and 70% for Innovation Actions (IA) led by for-profit entities, plus an additional 25% flat rate to cover indirect costs.

Complementing these funds, the implementation of the Strategic Projects for Economic Recovery and Transformation (PERTE) constitutes a milestone in the sector’s financial architecture, mobilising billions of euros for the modernisation of critical infrastructure. Despite the closure of some initial phases, the current Addendum to the Recovery Plan maintains the validity of this ‘financial lever’ through new calls for proposals and subsidised loan schemes for the period 2024–2026:

- PERTE Naval: with a public budget of €310 million, it offers direct grants and loans covering up to 40%–60% of costs related to digitalization and maritime sustainability.

- PERTE for Industrial Decarbonisation: mobilises €3.1 billion (with a recent call for proposals of €330 million in February 2026) and aid intensities of up to 60% for electrification and the use of hydrogen.

- PERTE VEC and PERTE Chip: with budgets exceeding €4.3 billion and €12.25 billion respectively, they finance the electric vehicle value chain and advanced sensor technology with grants of up to 40%.

This availability of funds supports the thesis of the analysis: R&D&I enables the raising of public capital to reduce the use of own funds (equity), transforming technological investment into a direct source of liquidity and tax savings.

Financial Efficiency through Tax Deductions

Spain ranks as one of the most competitive jurisdictions in the OECD in terms of tax incentives for innovation, thanks to the regulatory framework established primarily by Royal Legislative Decree 4/2004. Unlike grants, these deductions do not count as income in the tax base, but directly reduce the total Corporation Tax liability, offering an immediate impact on the project’s liquidity and profitability.

The key to a successful investment strategy lies in the correct technical distinction between R&D and IT:

- Research and Development (R&D): this category is reserved for projects involving an objective innovation and significant scientific or technical progress. In the port sector, this includes, for example, the design of new zero-emission propulsion systems or disruptive computer vision algorithms not previously available on the market. The basic deduction is25% of direct costs, but this can be increased through additional deductions for costs relating to qualified research staff (exclusivity) or for investments in fixed assets, potentially reaching an effective rate of up to 42%.

- Technological Innovation (TI): this is the most common route for companies in the logistics-port cluster. It applies to projects which, although not representing a world first, do involve a subjective innovation for the company through the substantial improvement of existing processes. The deduction is 12% and covers everything from the implementation of advanced terminal operating systems (TOS) to the re-engineering of loading and unloading processes through the integration of IoT sensors.

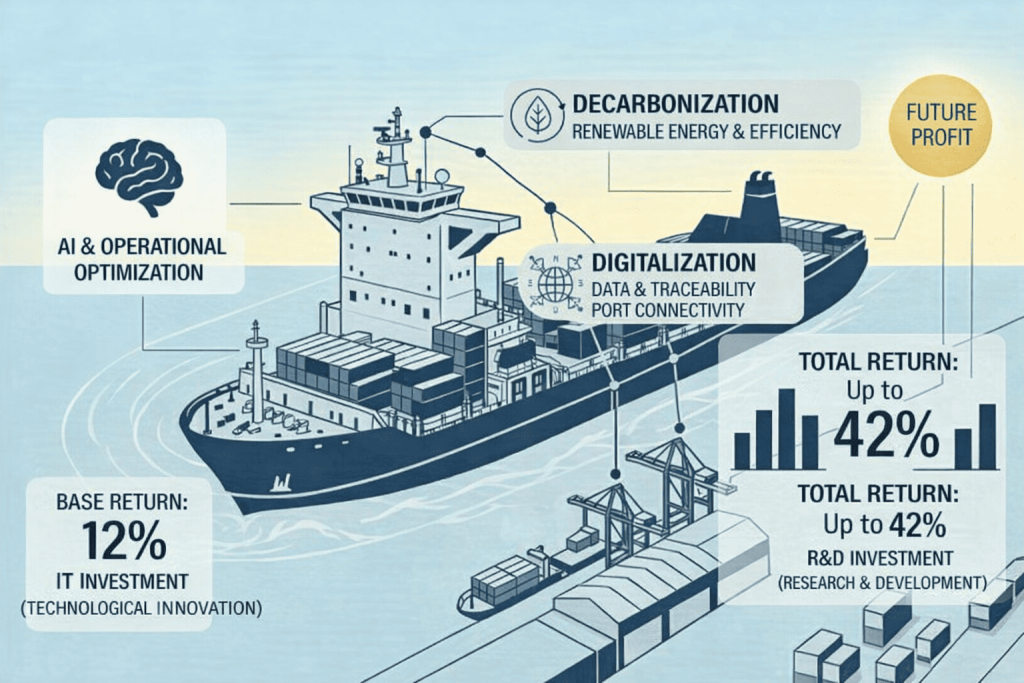

Illustration 3. Schematic of tax deduction returns in the port sector

Source: Own elaboration using AI

It is important to note that these incentives are compatible with the Social Security contribution relief for research staff, provided that the requirements of current legislation are met. Furthermore, for those companies that do not have sufficient tax liability to apply the deduction (for example, in early-stage investment phases or port-based start-ups), the legal framework allows, under certain conditions, for the monetisation of the deduction (the tax ‘cash-back’), by requesting direct payment from the tax authorities following the application of a 20% discount on the amount.

Furthermore, from a long-term planning perspective, the tax system offers critical temporal flexibility: deductions generated but not applied can be carried forward for a period of 18 years. This timeframe of almost two decades allows port operators and technology companies to generate ‘tax credits’ in years of heavy technical investment to offset them in future financial years with higher profitability.

This duality between tax savings and liquidity injection makes deductions an indispensable pillar for any strategic plan for digital or energy transformation in the maritime-port sector.

4. The Legal Certainty Framework

There are various ways to apply R&D&I tax deductions in corporation tax, ranging from simple self-assessment to binding rulings. However, in a complex regulatory environment, the route that provides the greatest legal certainty for a company is obtaining Binding Reasoned Reports (IMV). The IMV safeguards the technical classification and associated expenditure against future inspections by the Tax Agency.

The Technical Certification and Strategic Collaboration Process

This certification process must be led internally by the companies’ innovation and finance departments, working across organisational boundaries. However, given the technical complexity, the support of consultancies or entities specialising in incentive management is essential. These consultancies act as a link with ENAC-accredited bodies, such as ACIE or EQA, facilitating the preparation of reports that strictly comply with the requirements for the Ministry of Science and Innovation to issue the IMV.

5. Professionalisation of Management: Structure and Traceability

Efficient management not only ensures regulatory compliance but also enables the optimisation of the entire process and the maximisation of recoverable R&D&I expenditure. Without a clear structure, a large part of the company’s technical investment is diluted without being monetised.

Internal management structure: the Innovation Director and Controller

In a modern port organisation, the professionalisation of R&D&I requires the consolidation of two key roles whose synergy ensures the financial and viability of projects. On the one hand, the Innovation Director assumes strategic responsibility for the organisation and control of technical traceability. Their work is critical to ‘fortify’ project reports, ensuring that every technological milestone, engineering hour and test is documented to standards that successfully pass audits by certification bodies and funding agencies.

On the other hand, this structure is complemented by the role of the Innovation Controller, a technical-financial profile highly recommended for overseeing cost traceability. This professional acts as a guarantor that every expenditure item (staff, materials or external collaborations) is recorded in accordance with regulatory requirements, preventing a loss of profitability due to procedural errors in the supporting documentation. Together, these roles transform administrative management into a financial quality control process, ensuring that the project’s potential profit is consolidated as a real asset in the company’s accounts.

ISO 56001

This professional internal management structure finds its regulatory and operational backing in the implementation of international quality standards. The adoption of ISO 56001 (Requirements for an Innovation Management System) enables the partnership formed by the Innovation Director and the Innovation Controller to operate within a framework of standardised and auditable processes.

Beyond being a mark of reputational recognition, certification to this standard ensures that the collection of technical evidence and cost traceability adhere to a methodological rigour that is irrefutable before the authorities. In this way, ISO 56001 acts as the mechanism that ensures the ‘financial lever’ functions with precision, minimising the risk of discrepancies in audits and consolidating the culture of innovation within a company as a robust, predictable and, above all, profitable business process.

However, for this architecture to be truly effective, innovation management cannot operate as an isolated department; it must be fully integrated into the company’s overall management systems and strictly aligned with its strategic plan. It is no coincidence that its implementation can be validated by an accredited certification body — such as Bureau Veritas, amongst others — which transforms innovation into a standardised process, turning isolated creativity into a predictable, auditable and high-performing business process.

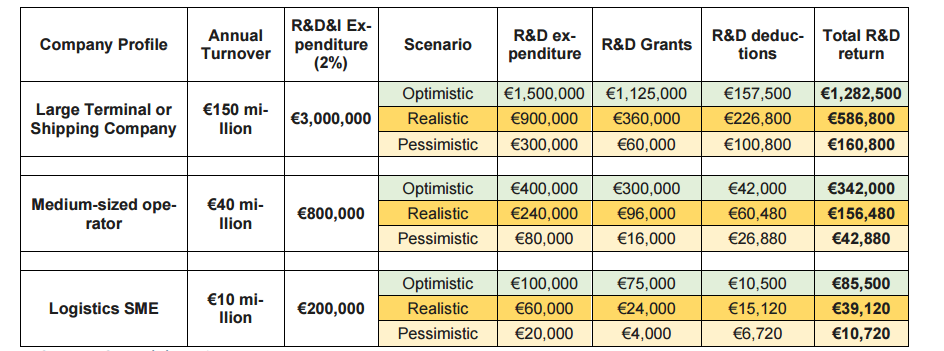

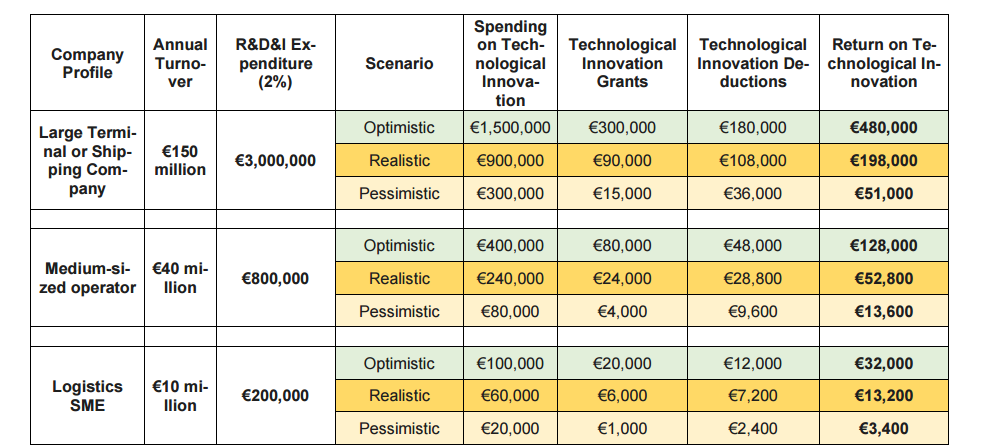

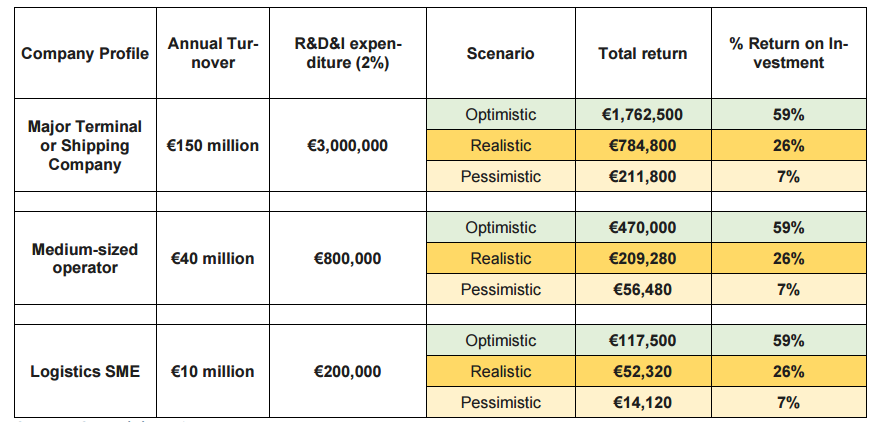

6. Financial Forecasting and Profitability Scenarios

Below are three return scenarios based on current Spanish regulations. It is important to note that these are estimated models; the final outcome depends on the technological intensity of the activity carried out and the organisation’s financial strength.

In the port sector, company size is a critical factor of scale: whilst large terminals and global operators have the necessary investment capacity and to undertake disruptive infrastructure projects (such as full automation or green hydrogen), logistics SMEs tend to focus on process innovations or digitalization (software). However, the legal framework balances this by allowing SMEs access to deduction rates and subsidies that are occasionally higher. Furthermore, the nature of the project — whether it qualifies as R&D (objective novelty) or as IT (subjective novelty for the company) — will determine whether the return approaches the maximum tax savings brackets.

Table 1. Estimated return on R&D (tax deductions and grant income) for the port sector

Source: Own elaboration

Table 2. Estimated return on technological innovation (tax deductions and grant income) for the port sector

Source: Own elaboration

Table 3. Estimated total return (R&D&I) including tax deductions and grant income for the port sector

Source: Own elaboration

7. The Innovation Ecosystem: integration and synergies with stakeholders

Success in the field of port R&D&I is not achieved through isolated efforts, but depends on organisations’ ability to integrate into an open innovation model. The complexity of current challenges — such as the energy transition or Industry 4.0 — demands close collaboration with the various stakeholders that make up the knowledge value chain. This network of partnerships helps to spread technological risk and accelerate the time-to-market of the solutions developed.

Within this ecosystem, the key players fall into the following strategic categories:

- Universities and technology centres: these represent the source of scientific knowledge and basic research. Their collaboration is essential for the transfer of technology towards practical applications in the port environment, enabling advances in areas such as materials science or advanced algorithms to become operational solutions.

- Specialist consultancies: act as strategic partners in the financial and fiscal architecture of projects. Their work is critical to ensuring the viability of investments through the design of public funding strategies and the correct structuring of applications aimed at securing tax benefits.

- Engineering firms, research centres and foundations: act as catalysts for collaborative projects, facilitating the creation of international consortia and research networks and access to glob e best practices. Their ability to connect the industry’s real needs with suppliers’ technical capabilities makes these institutions the linchpin of the innovation system. Entities such as foundations linked to port authorities play an essential catalytic role in this environment.

- Technology companies and start-ups: the integration of agile technology providers enables large terminals and operators to incorporate disruptive innovations more rapidly. The port thus acts as a living lab where prototypes are validated in real-world operating environments.

It is the coordination of these stakeholders, within a clear governance framework, that enables individual projects to be transformed into a genuine cluster strategy, positioning the port system as a global benchmark for efficiency and sustainability.

8. Conclusion

The maritime-port sector faces a major opportunity. Strategic investment in R&D&I —driven by Artificial Intelligence (AI), decarbonisation and comprehensive digitalization— is not only a vehicle for operational modernisation, but also acts as a direct catalyst for improving the bottom line. To achieve maximum competitive potential, it is imperative to professionalise innovation management, integrating it into the corporate structure as a cross-functional business unit.

This approach must be underpinned by the legal certainty provided by Binding Reasoned Reports (IMV) and by an internal management methodology aligned with international standards, such as ISO 56001. Ultimately, those organisations capable of forging robust alliances within their stakeholder ecosystem will be the ones leading the way in profitability and innovation within the global logistics transport sector.

References

- EUROPEAN COMMISSION. 2025. The 2025 EU Industrial R&D Investment Scoreboard. Luxembourg: Publications Office of the European Union. JRC144638. Available at: https://iri.jrc.ec.europa.eu/scoreboard/2025-eu-industrial-rd-investment-scoreboard [Accessed 26-02-2026].

- COTEC FOUNDATION FOR INNOVATION. 2025. Cotec Report 2025: R&D&I in Spain. Madrid: Cotec. Available at: https: //informecotec.es/ [Accessed 20 February 2026].

- MARKETSANDMARKETS. 2023. Artificial Intelligence in Logistics Market – Global Forecast to 2027. Pune: MarketsandMarkets Research Private Ltd. Available at: https://www.marketsandmarkets.com/Market-Reports/artificial-intelligence-in-logistics-market-120021876.html [ Accessed 27-02-2026].

- INTERNATIONAL ORGANISATION FOR STANDARDISATION (ISO). 2024. ISO 56001:2024 Innovation management — Innovation management system — Requirements. Geneva: ISO. Available at: https://www.iso.org/es/contents/data/standard/07/92/79278.html [Accessed 26-02-2026].

*Disclaimer: This English version has been generated with the support of AI-based translation tools. In case of discrepancies, the Spanish original prevails.