The monetary policy dilemma: the game must change

A world of permanent monetary laxity

The situation unfolding in the Persian Gulf, particularly in the Strait of Hormuz, once again presents central banks with an age-old dilemma, one that is always complex to resolve: a supply shock that restricts economic growth (requiring monetary expansion) but, at the same time, generates inflationary pressures (requiring a restrictive policy).

As Christine Lagarde, President of the European Central Bank, rightly pointed out at the start of the conflict, monetary authorities may adopt a wait-and-see approach provided the conflict is brief and does not significantly alter energy prices; if these rise sharply, even if not for long, the tone will have to harden, and this must be accompanied by some rise in interest rates (the current scenario).

If the energy shock is not only intense but also prolonged, central banks will have to adopt a more restrictive stance to prevent inflation from becoming entrenched through second-round effects, with a feedback loop between factor prices (including wages) and the prices of goods and services that could cause serious problems in the medium term.

This approach is the correct one… but not the one the monetary authorities adopted the last time they faced this dilemma. Apparently, the lessons of the inflationary spiral of the 1970s had already been forgotten. Thus, in a highly unfortunate interpretation of the implications of the events of 2020–2022 (the COVID-19 pandemic, the invasion of Ukraine and the ultra-expansionary policies adopted in response to these shocks), Western central banks (unlike those in many emerging economies, which had tightened their monetary policies earlier) considered this to be a short-term supply problem.

In reality, neither could the production and supply difficulties be resolved in the short term, nor did it make sense to ignore the demand-side pressures arising from those very policies and from the accumulated savings (both voluntary and forced) during the toughest moments of the pandemic.

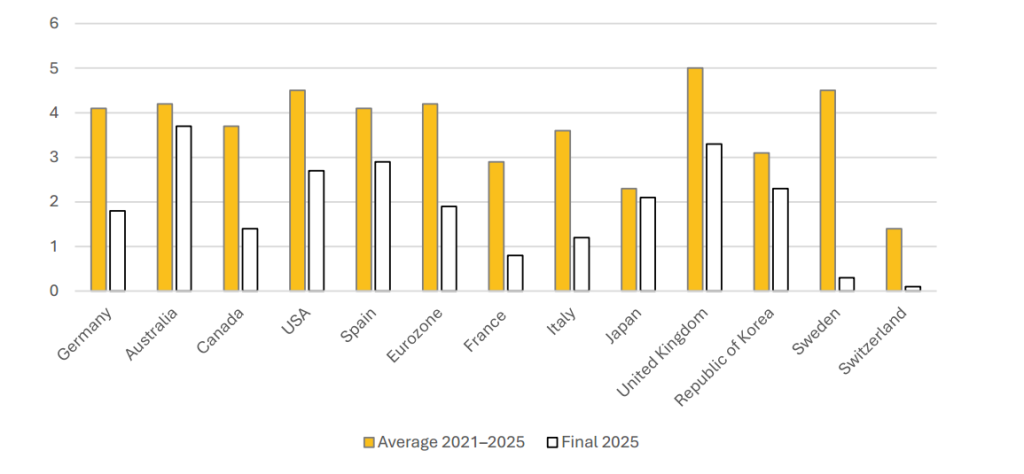

This misreading of reality led to a significant delay in the start of interest rate hikes, which were necessary to prevent inflation from becoming entrenched. Despite the intensity of that cycle of rate rises once it began, average inflation rates for the five-year period 2021–2025 (see Graph 1) have been well above the 2% annual increase in prices that tends to be defined as ‘price stability’, and around which the inflation targets of Western central banks are set.

Graph 1. Inflation rate (CPI; %)

Source: Own compilation based on data obtained from the Bank for International Settlements (BIS)

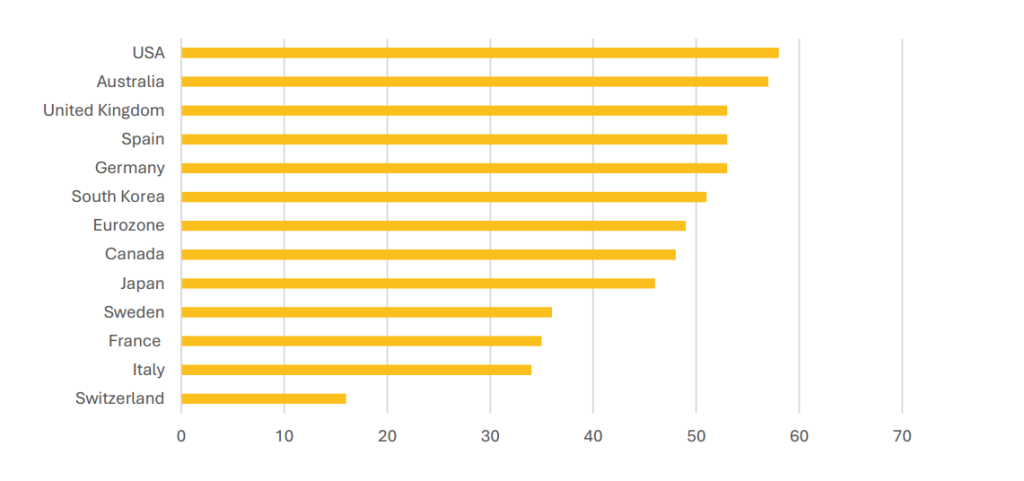

It is true, as Graph 1 itself reveals, that by 2025 average inflation rates in most (though not all) Western economies have returned to levels close to, or already fully in line with, the aforementioned target. However, failure to meet this target over the past five years has been the norm (with the exception of Switzerland), and even where it has not been almost permanent, as shown in Graph 2.

Graph 2. Number of months with year-on-year inflation above 2% between January 2021 and December 2025

Source: Own compilation based on data obtained from the Bank for International Settlements (BIS)

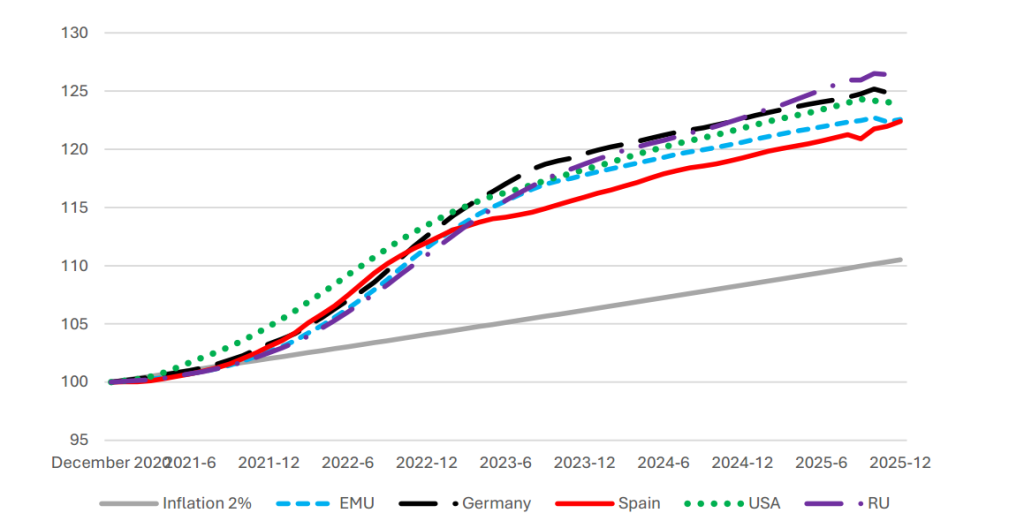

More importantly, particularly in terms of public disaffection (and, according to all polls, the public’s anger over the rising cost of living has had serious electoral repercussions, from Japan to Germany, from the UK to, most notably, the United States), what matters to people’s pockets is not the year-on-year rate at any given moment, but the cumulative impact on price levels over time.

As shown in Graph 3, from the end of 2020 to the end of 2025, the deviation from the target (2% per annum) has been between ten and five percentage points (despite the fact that the first few months of 2021 were still characterised by price stagnation), and not all groups in developed countries have seen their incomes rise by an equivalent amount (above 2% per year) during this period. Given that particularly sensitive (and frequently purchased) items, such as energy and food, have become more expensive than the average, discontent over price trends has spread amongst Western citizens.

Graph 3. Consumer prices (CPI; cumulative change; 2020:12 = 100)

Source: Own compilation based on data obtained from the Bank for International Settlements (BIS)

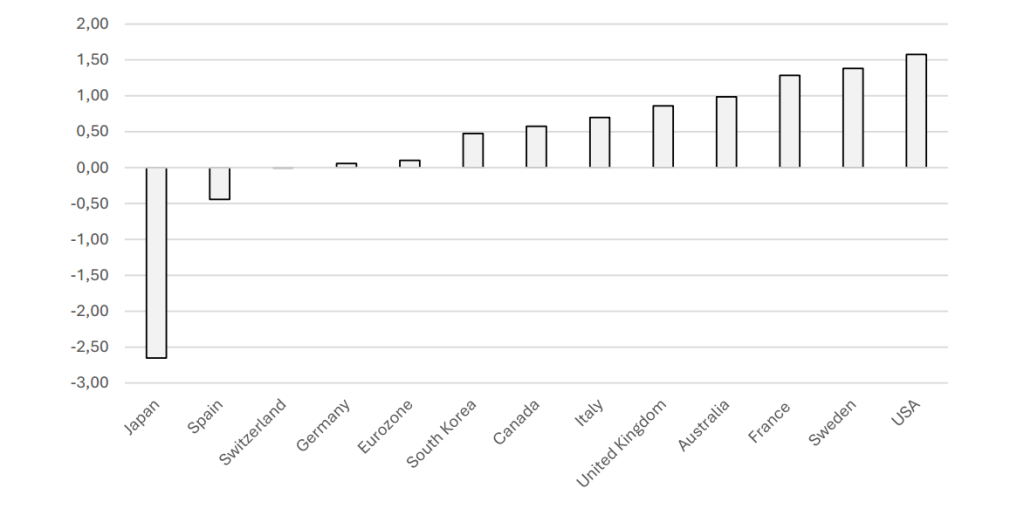

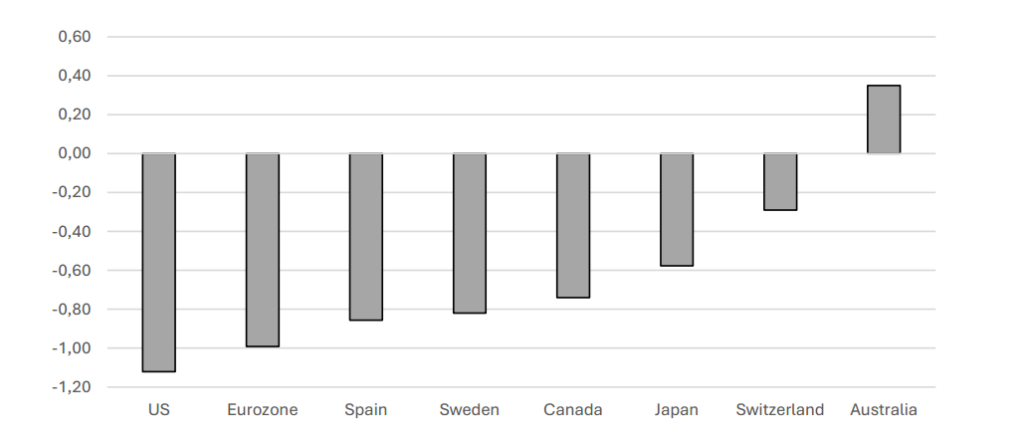

Despite this, it cannot be said that monetary policy in developed countries is currently even neutral, let alone restrictive. Graph 4 shows real interest rates (calculated as the central bank’s reference rate minus the year-on-year inflation rate) in the major developed economies, and it can be seen that, in most cases, these rates are negative or close to zero. Even for countries with the tightest monetary policy, the real rate is below what was typical in the decades prior to the Great Recession.

Graph 4. Real interest rate (2025 average; %)

Source: Own compilation based on data obtained from the Bank for International Settlements (BIS)

But monetary policy is not driven solely by interest rates. Precisely in the wake of the financial crisis and its subsequent ramifications, central banks began (imitating what, admittedly with little success, had been practised in Japan since the 1990s) an increasingly vigorous foray into so-called unconventional monetary policy which, without going into technical details, ultimately manifests itself in an expansion of the monetary authorities’ balance sheet (or, in simple terms, the injection of more money into the economy).

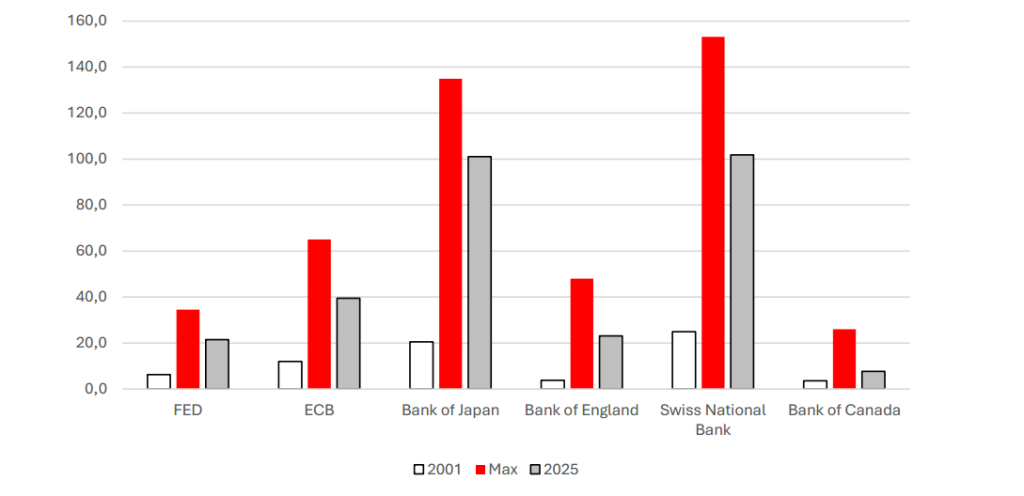

More than fifteen years after its widespread adoption, this growth in balance sheets is far from having been reversed… nor does it show any signs of doing so. Graph 5 shows, again for the major developed economies, the size of central bank balance sheets as a percentage of GDP (i.e. taking into account that, logically, when the economy grows, the money supply must also do so) prior to the Great Recession, in 2025 and at their historical peak, generally in 2020 or 2021, given that the response to the pandemic involved the largest monetary injection ever undertaken.

It is true that, relative to that peak, and as part of the tightening cycle of 2022–2024, there has been a downward correction which, however, has stalled in recent quarters. This leaves us with a balance sheet size that is between double (Canada) and six times (United Kingdom), and more than triple for both the United States and the Eurozone, that of the central bank’s balance sheet prior to the start of the ‘reign’ of unconventional monetary policy.

Graph 5. Total central bank assets (% of GDP)

Source: Compiled by the author based on data from the Bank for International Settlements (BIS)

The picture of the current situation is now complete, but it is important to understand why we have reached this point, why it is problematic, and how this situation can be changed in a sustainable manner. Let us proceed to do so.

“The only game in town”

It can be argued that monetary policy in the West has been asymmetric (swift and sharp interest rate cuts at the slightest hint of recessionary scenarios, and delayed and gradual hikes in the face of inflationary threats) since the turn of the century, with the response to the bursting of the dot-com bubble or the 9/11 attacks. In any case, it was in the wake of the Great Recession that monetary policy became the lifeline of the economy (and central bankers little short of heroes to the rescue).

Faced with a crisis unprecedented in developed economies since the Second World War, with fiscal policy constrained by uncorrected budgetary imbalances from the previous expansionary cycle, counterproductive and conflicting exchange rate interventions (with multiple countries seeking to devalue their currencies to boost exports) and insufficient structural reforms implemented in most economies, monetary policy remained, in Mohamed A. El-Erian’s apt and now famous definition, as “The Only Game in Town”, that is, as the sole line of defence against a recession of such severity.

And there is almost unanimous agreement that the monetary authorities did their job. First with the conventional approach (cutting interest rates to the lowest possible level) and, when that proved insufficient, by resorting to unconventional policies, ranging from the expansion of liquidity provision across the board to the modification of the yield curve, from the purchase of assets—primarily government debt, but also private debt—to forward guidance, or the commitment to maintain the exceptional monetary expansion over time. Undoubtedly, the crisis was shortened by these policies, which brought about greater growth and lower unemployment.

The problem is that what was meant to be exceptional became the norm. Firstly, due to the overwhelming support—political, popular and from a high proportion of experts—for this monetary laxity, even though almost all analysts came to recognise that the marginal benefit of each expansionary measure was diminishing. Secondly, because of a certain tendency among monetary authorities to be content with the status quo, refusing to accept (with the honourable exception of the Bank for International Settlements) that such permanent monetary easing entailed significant problems.

And, thirdly, because the supposed main cost of that policy—inflation in goods and services—was not materialising (thanks to Asia’s boundless productive capacity, technological progress—ICTs—and the extreme efficiency achieved across the various links in the global supply chain). Thus, during a decade of sustained economic expansion, not only did the size of central banks’ balance sheets fail to normalise, but the real interest rate was negative for most of the period (see Graph 6).

Graph 6. Real interest rate, average 2011–2019 (%)

Source: Author’s own calculations based on data from the Bank for International Settlements (BIS)

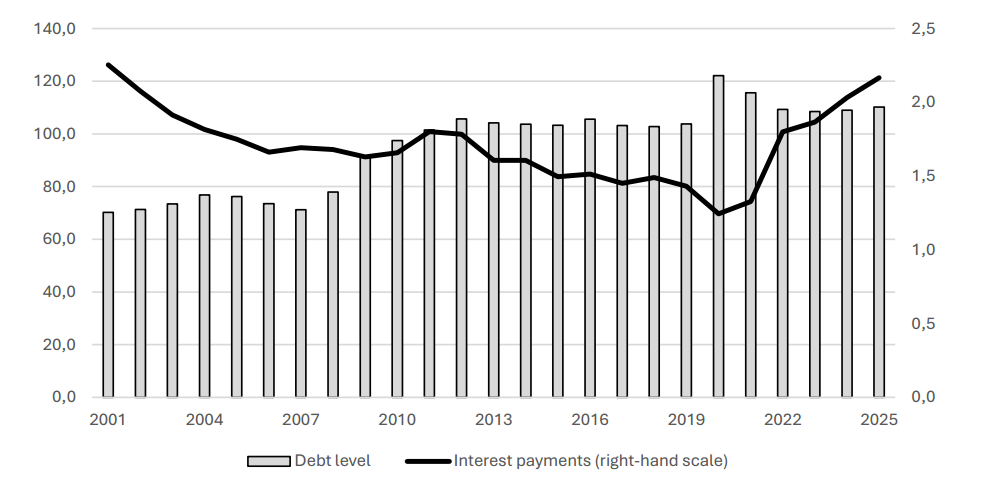

Western governments found this monetary environment particularly favourable. Whilst their debt continued to rise, the cost of that debt fell (Graph 7), driven by sustained demand from central banks and the fact that interest rates remained remarkably low across all segments of the yield curve. With environmental, demographic and political challenges (the rise of populism) dominating public attention, what better option for these governments than to increase spending without raising taxes, at virtually (or, for countries such as Switzerland or Germany, almost entirely) zero budgetary cost.

Graph 7. Developed countries: level of gross public debt and interest payments on it (% of GDP)

Source: Own compilation based on data from the International Monetary Fund

When the COVID-19 pandemic pushed the global economy to the brink of collapse (largely due to necessary voluntary measures to reduce the disease’s toll on human lives), the macroeconomic response was clear: more of the same, but with greater intensity.

Maximum fiscal profligacy in peacetime, accompanied by monetary expansion (largely to finance fiscal schemes involving higher spending and lower taxes) unprecedented in any era (see again Graph 5 to observe the increase in the size of the monetary authorities’ balance sheet). But the good times came to an end. The old forgotten spectre (inflation in goods and services) returned, and with it, criticism began to intensify regarding some of the other costs of the flood of almost free liquidity that the West had been experiencing for over a decade.

Time to face reality

Indeed, as already noted, Western central bankers interpreted the excessive price pressures that had already emerged in 2021 as stemming exclusively from supply shocks (COVID-19 and the invasion of Ukraine), with the well-known repercussions on trade flows, supply chains and energy costs. And, of course, central banks lack the tools to combat this type of disruption, which, moreover, with surprising determination, they described for months as ‘transitory’.

Although one might feel some sympathy for the authorities facing these exceptional situations, their inaction was hardly appropriate. Firstly, quite a few experts warned that frictions in global value chains would persist for years (for example, the shortage of shipping capacity until a considerable number of new vessels came into service).

Secondly, if the 1970s taught us anything, it is that, however much inflation may stem from the supply side, if it becomes entrenched, widespread and feeds into market participants’ expectations, restoring price stability may require raising interest rates to considerable levels.

Thirdly, it is hardly credible that central banks, particularly but not exclusively the US Federal Reserve, were unaware that the more than twenty trillion dollars of fiscal and monetary expansion introduced in the West in response to the pandemic also generated demand-side pressure on prices, which not only increased dramatically with the recovery but also shifted unevenly (more towards goods, less towards services) as a result of changes in mobility and in citizens’ spending possibilities due to the fight against COVID-19 itself.

The return of the spectre of inflation, which has still not been fully exorcised (and even less so, in fact quite the opposite, given the events surrounding the Strait of Hormuz), must not make us forget that permanent monetary laxity has other costs, which have been ignored over the past decade. It would be wise to remember them.

It is, for example, abundantly clear that this policy penalises prudent saving. Real interest rates close to zero (or even below) mean that investing in relatively safe assets results in a loss. Taking on additional risks to achieve a certain return is particularly worrying when done by parties with limited capacity to understand the implications of such a move.

When this coincides with a period, such as the current one, in which tempting innovations, such as crypto-assets, are emerging, the losses for individual investors without sufficient training can be significant. And it should not be overlooked that, even with ample financial knowledge, there are entities (pension funds, insurance companies) that are sometimes faced with the need to achieve committed returns, and can only do so, due to very low interest rates, by increasing the risk they have traditionally assumed.

Of course, the abundance of cheap money has a general upward effect on the value of all types of assets, not only the (relatively) new ones, but also real assets (particularly housing) or traditional financial assets, whether fixed-income or equity.

The deviation of asset valuations from what is justified by the underlying fundamentals of supply and demand (i.e. the formation of bubbles) does not usually end well. The last major disconnect between price stability for goods and services (much to the satisfaction of central banks) and high asset inflation (which the authorities chose to ignore) culminated in the very severe Great Recession. And it does not seem difficult to identify overvalued markets today.

Linked to the above is an additional problem, also easy to grasp, although, at a time when inequality has become a major concern for the public, it is vehemently denied by some monetary authorities: ultra-expansionary monetary policies increase inequality in the distribution of wealth, insofar as they inflate the prices of assets that are, of course, for the most part owned by the highest strata of society. This does not prevent us from recognising that this same policy, insofar as it helps to reduce unemployment, particularly in times of crisis, improves income distribution; however, its impact on wealth is the opposite.

Another cost, particularly relevant from a structural perspective, of prolonged and extreme monetary laxity is that it facilitates the practice of ‘evergreening’, that is, banks extending new loans on favourable terms to borrowers who face serious difficulties in maintaining their operations profitably.

In particular, these loans to companies with no future have led, over the past decade and a half, to the proliferation of “zombie firms” (formally, those that do not earn enough even to cover the interest on past debts), alongside the corresponding “zombie jobs”.

This not only amounts to an absurd postponement (increasing final costs) of the company’s bankruptcy, but also hinders access to a sector for new and better business projects and/or diverts funds from promising (sub)sectors to others with little future viability. The impact of this deadlock on productivity is significant, and it hinders the shift towards a more robust growth model, one not underpinned by rising debt and cheap money.

We shall conclude (without claiming to be exhaustive, since, for example, we could also expand on the costs to emerging and developing countries of such loose monetary policies – and their reversal – in the West) this reflection on the problems of continuous monetary expansion with its implications for the independence of central banks.

A long tradition, both theoretical and empirical, regarding the benefits of such autonomy—at least in the design and implementation of monetary policy (with the policy objective either delegated to the independent authority or defined by the government, and always with the Central Bank being obliged to account for its actions in exchange for functional independence) gave way, from the early 1990s onwards and progressively, to all developed economies – and a significant number of the rest – accepting the desirability of such independence.

Despite criticism regarding the inappropriateness of conferring such power on an ‘unelected’ authority, the inflationary and even hyperinflationary disasters caused by central banks acting in the service of the government of the day suggested that the independence of the monetary authority from political power was here to stay.

However, the monetary policy pursued since 2008 opens up three potential avenues of attack on that independence: the losses that may arise from massive purchases of government debt, the setting of objectives that do not correspond to those traditionally pursued by a central bank, and a potential situation of ‘fiscal primacy’ in developed countries.

Firstly, the purchase of trillions of dollars (euros, yen, Swiss francs, pounds, etc.) of public debt, generally at high prices, to make its sale attractive to private investors (particularly banks, which were supposed to use the liquidity received to increase lending to households and SMEs), means that, upon the maturity of that debt, monetary authorities are losing significant amounts of money. However, for the currency issuer, these losses can be deferred and offset by the usual positive results of the monetary authorities, without having to rely on government transfers that threaten their independence.

The second approach mentioned is more delicate. If central banks abandon their macroeconomic objectives (always price stability, accompanied, on occasion and depending on the country, by others linked, for example, to employment or exchange rates) and financial (contributing to the stability of the system, particularly the banking system) and venture into other areas ostensibly far removed from their conventional mandate (social, environmental, governance), they become open to criticism from those opposed to the definition of these other objectives. Furthermore, it is highly debatable whether multiplying priorities helps central banks achieve their core objectives.

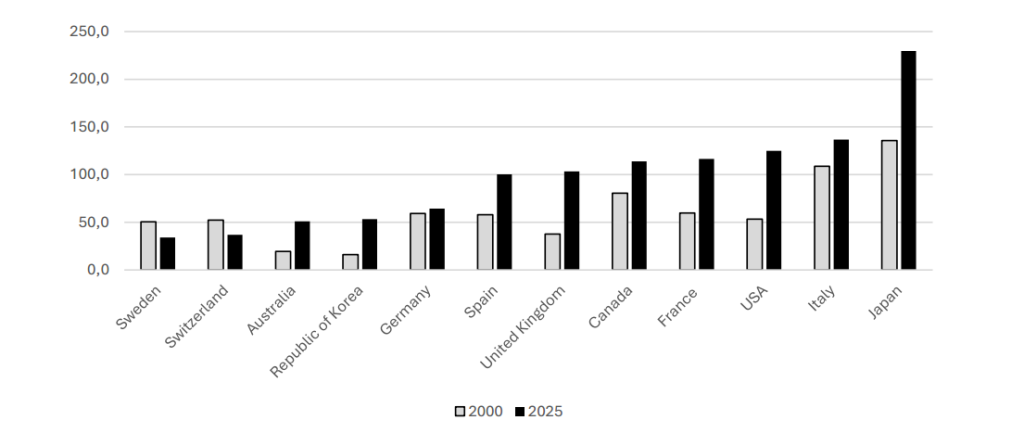

But where the real risk to the independence of monetary authorities (and the significant benefits that societies derive from it) lies is in their potential subjugation by heavily indebted governments. Graph 8 shows how public debt in developed countries has skyrocketed in this century (even when, as is appropriate, adjusted for the larger size of the economies), with few exceptions (concentrated in central and northern Europe) reaching double or even triple the levels of the year 2000.

Graph 8. Gross public debt (% of GDP)

Source: Author’s own calculations based on data from the International Monetary Fund

As debt accumulates, the temptation to succumb to ‘fiscal primacy’ increases in parallel. This is a situation in which the primary objective of monetary policy is to guarantee the government’s solvency by stabilising the real value of its debt; consequently, inflation is determined by the needs of fiscal policy (inflation higher than that compatible with price stability reduces the real value of public debt and promotes its sustainability).

Such a scenario usually ends with rising prices, a loss of investor confidence (misled by inflation that does not compensate them) and greater medium- and long-term problems for governments than the short-term benefits gained. But let us not forget that the political cycle is very short in the West.

More than one analyst considers that, in reality, a certain deference to the interests of governments explains the extraordinary monetary laxity between 2009 and 2021 that we have highlighted in this analysis. Recall once again Graph 7 and how higher levels of debt were strikingly accompanied by a lower cost (in terms of GDP) of that debt. But note also how, with the (at least partial) normalisation of interest rates since 2022, interest payments have risen significantly in recent years.

In short, we have seen that the costs of a permanently expansionary monetary policy (which, moreover, has been increasingly so, at least until 2021) are significant enough not only to warrant consideration, but also to outweigh, perhaps by a considerable margin, the benefits derived from it. We cannot continue down the same path.

Towards a new and balanced model

Deep down, all stakeholders and decision-makers are aware that economic growth in developed countries over the past two decades has been underpinned by an unsustainable accumulation of debt (public and/or private, depending on the period), facilitated by the vast amounts of cheap money injected by central banks as the only recourse (“the only game in town”) to sustain that growth, however precariously.

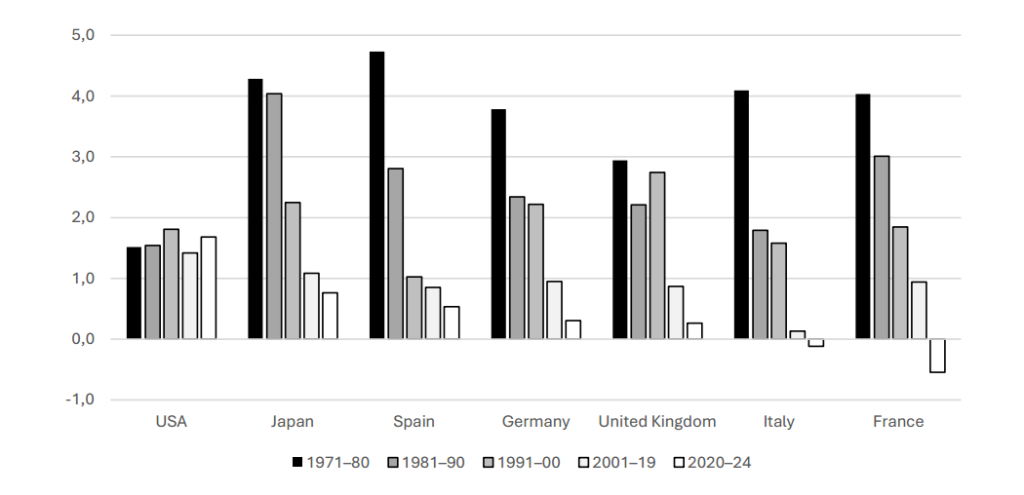

As Graph 9 reveals, the trend in the key driver of economic progress from the late 18th century to the late 20th century – labour productivity – has become a real cause for concern, with only the United States offering at least a partial exception among these developed countries.

Graph 9. Productivity per hour worked (average annual change, %)

Source: Own compilation based on data from the Organisation for Economic Cooperation and Development (OECD).

The time has come (it would have been better years ago, but the past cannot be changed) to replace continuous monetary injections with more solid foundations for growth. Central banks must emphasise the need for this change and act accordingly, with less asymmetry in interest rate decisions, a gradual reduction in the size of their balance sheets, and a focus on achieving their conventional objectives. But the responsibility of the governments of rich economies (and many others) is even greater, in two crucial respects.

On the one hand, a comprehensive and intelligent review of their fiscal policies, recalibrating revenue and expenditure so as to increase those linked to driving sustained and sustainable growth and reducing superfluous and inappropriate spending, as well as excesses in current expenditure, which may be politically convenient but economically detrimental.

The reduction in the debt burden resulting from this ‘ ’ cut will allow for a reduction in interest payments on the debt and the allocation of those funds to expenditure that does indeed seem unavoidable, such as that arising from demographic ageing.

Much of this would be facilitated if economic growth were underpinned by essential structural reforms that have long been deferred, either because they are complex, because they are politically complicated (for example, if they involve ceding sovereignty to a supranational institution), or because they disadvantage vocal minority groups opposed to them, as opposed to a broad majority of beneficiaries who are not organised to support them.

In the European case, the European Commission’s inability (not so much due to a lack of will on its part, but rather due to opposition from national governments) to complete the Single Market imposes costs on businesses and citizens that far exceed those arising from the protectionism of any trading partner. The exemplary reports led by Enrico Letta and Mario Draghi (whose recommendations are being implemented slowly and to a limited extent) reveal how the lacklustre growth of EU countries could be decisively revitalised.

More generally, the formulae for accelerating productivity growth are well established: reducing barriers to business creation and, thereby, to wealth creation; boosting funding, through various forms of venture capital, for innovative projects, with a particular focus on innovation at the technological frontier; intensify the dissemination of these frontier technologies to the rest of the economy; train managers and workers to be able to make the most of these new technologies.

Improve physical and technological infrastructure, with public-private partnerships as a desirable approach; guarantee intellectual property rights (while limiting their abuse) and access to public procurement in a balanced manner; strengthen education geared towards the new demands of the labour market, not only within the formal education system but also through in-service training; or by improving the matching of workers to jobs, providing sufficient information and promoting mobility…

The new technological wave, led by Generative Artificial Intelligence and extending to quantum computing, genetic engineering, advanced robotics, new materials, space exploration, amongst other fields (one might add, now that it has made the leap from experimentation to widespread use, nuclear fusion), offers a unique opportunity to revitalise economic growth driven by rising productivity rather than cheap money. But it also demands immediate and vigorous action from all stakeholders to seize this opportunity.

Curiously, to the extent that it drives economic growth, raising investment above savings, AGI (along with other new technologies) will lead to higher interest rates than those seen recently in the medium and long term, in line with historical patterns (long-term rates and growth in productivity and output have always moved in parallel), and will help to rebalance the excessively expansionary monetary stance of recent decades.

Conclusions

The monetary policy pursued by central banks since at least 2008 has been characterised by extreme laxity, which has been increasing (up to 2022) and, on more than one occasion, excessive. The cumulative costs of this policy, without even waiting for the surge in inflation of goods and services experienced in the three-year period 2022–2024, have been very significant, and are very likely to exceed the benefits of maintaining it.

But it is true that, with economic growth underpinned by rising levels of leverage, requiring cheap money so that this mounting debt does not bankrupt public and private agents, a shift in the stance of monetary policy cannot be carried out in isolation, at the risk of suffering prolonged economic stagnation.

Monetary normalisation (in terms of interest rates and balance sheet size) by central banks must be accompanied by a more intelligent fiscal policy and, no less importantly, by the implementation of the structural reforms necessary to unlock the full potential accumulated in economies, particularly at a time when the new technological wave promises to restore the great historical foundation of wealth and development: the advancement of labour productivity.

References

- Akarsu, O. et al. (2025); “Zombie firms in networks: Congestion and evergreening”, Economic Modelling, volume 151. October.

- Alburquerque, B. and Iyer, R. (2024); “The rise of the walking dead: Zombie firms around the world”, Journal of International Economics, volume 152.

- Álvarez, L. et al. (2023); “Distressed firms, zombie firms and zombie lending: a taxonomy”; Journal of Banking and Finance, volume 149.

- André, C. and P. Gal (2024), “Reviving productivity growth: A review of policies”, OECD Economics Department Working Papers, No. 1822, OECD Publishing, Paris.

- Bernanke, B.; Geithner, G. and Paulson Jr., H (2019); Firefighting: The financial crisis and its lessons. Penguin Books.

- BIS (2012); “Threat of fiscal dominance?”, BIS papers No. 65.

- Borio, C. (2019); “Central banking at challenging times”, speech at the SUERF Annual Lecture Conference on “Populism, Economic Policies and Central Banking”, November.

- *Consult the downloadable document for the complete list of bibliographic references.

*Disclaimer: This English version has been generated with the support of AI-based translation tools. In case of discrepancies, the Spanish original prevails.